With the so-called patent cliff looming, Julie Altier, of London-based strategy and marketing consultants Simon-Kucher & Partners, looks at the role of generic medicines in national healthcare strategies across the world.

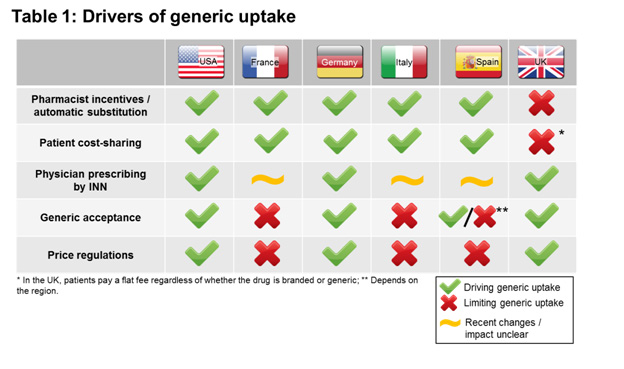

As generics are attractive cost-saving options, it is no surprise that they are at the centre of several current and future healthcare reform policies. Most governments have implemented policies and programmes that provide physicians with incentives to prescribe generics and pharmacists with incentives to substitute brands for generics.

In some cases, such as the US, Germany and the UK, these policies have succeeded in promoting generic use. In other markets, they have been less successful in promoting generics and have focused more on lowering overall expenditures. Therefore, brand prescribing remains high in these markets even after loss of exclusivity (LOE).

New and stricter policies have recently been implemented in some markets so the outlook may change in the next few years. This article explores why these policies have had unequal success so far across markets and examine how new policies seek to reverse this trend.