Is your company a price taker or a price maker? When given the choice, every business would choose to be a price maker; however, the choice is not the business’s to make. Whether your company is a price taker or a price maker is determined by the competitive environment of the market in which you operate. For instance, in a perfectly competitive market all firms are said to be price takers because no one firm has the power to change the market price.

Conversely, in a monopolistic market the firm is said to be a price maker since the market price of a product will equal the price level chosen by the monopoly.

A successful business plan is one that is dynamic and has the flexibility to adapt to changing market conditions

While companies do not control whether they are a price taker or a price maker, they do control their level of profitability through strategic decision making. A successful business plan is one that is dynamic and has the flexibility to adapt to changing market conditions. However, even a well thought-out, dynamic business plan is virtually useless if the key decision makers fail to recognise changes in the market as they happen.

Over the past three years, mergers and acquisitions (M&A) in the pharmaceutical outsourcing market have increased in frequency. While these movements are almost always highly reported in the media, what is often missed is the scope of the changes to the market – the big picture.

Individually, these mergers and acquisitions have a relatively small effect on the competitive environment of the market; yet, as a whole and over time, these M&As can affect the market structure itself. Just as speed to market is the pinnacle of considerations in getting a new drug to patients, the speed with which a company adjusts to structural market changes can be the difference between success and failure.

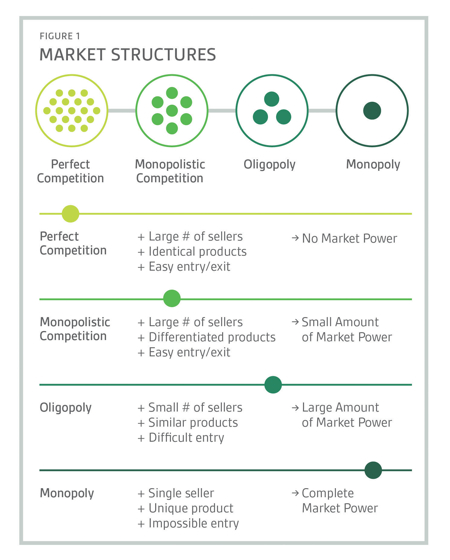

Figure 1 depicts four common market structures and highlights the major differences between each type. This graphic is useful in conceptualising the expected changes to a market environment as the market structure itself changes. As Figure 1 shows, perfectly competitive markets have a large number of sellers offering identical products with very low barriers of entry to the market.

The classic example here is the market for commodities (grains, corn, etc.). In this market, no one seller can raise the price of their product because, due to the identical nature of the products being sold, buyers will always opt to go for the lowest-priced provider. Similarly, no seller can lower the price of their products (in an effort to gain market share) since the extremely low barriers to entry facilitate fierce competition within the market, placing constant pressure on the sellers in the market to minimise costs, which translates into profit minimisation.

At the other end of the spectrum are monopolistic markets, which are defined by having a single seller, a unique product, and very high barriers to entry. In this market the seller can charge any price for their product without fear of competition because the unique product offered by the monopoly is typically covered under patent protection. Even if a company would like to offer a similar product (think Microsoft Zune vs Apple iPod), the barriers to entry in this market discourage increased competition either by fixed costs (i.e. costs associated with production and manufacturing) or by time (i.e. the cost of time for licensing, inspections, certifications, etc.). This time component can become more important in the pharmaceutical manufacturing sector due to the increased regulatory oversight required.

In the ‘real-world’, perfectly competitive markets and monopolised markets are extremely rare with the vast majority of markets around the world being classified as Monopolistic Competition or Oligopolies.

In the ‘real-world’, perfectly competitive markets and monopolised markets are extremely rare

Since we’re talking about mergers and acquisitions in the pharmaceutical manufacturing market the ‘Sellers’ are the CMOs and the ‘Products’ are the services offered by the CMOs. The more M&As in this market, the fewer the total number of sellers; thus from this insight alone we can envision the market structure moving to the right in Figure 1, thus CMOs are gaining in market power. To be clear, this increase in market power is true for all CMOs in the market, not just those who have experienced a recent merger or acquisition.

So what does this mean for your business? Speaking specifically of the pharmaceutical manufacturing equipment industry, equipment companies will be forced to give up some of their profit margins when dealing with CMOs because this increase in the CMOs’ market power translates into an increase in negotiating power – as there are now fewer companies to which the equipment companies can sell.

For a company to be successful in this newly formed market, an emphasis should be placed on customer satisfaction levels, customer retention, and repeat business. As a note, the total demand for pharmaceutical equipment is not expected to see a significant change following mergers and acquisitions; but the fact that there will now be fewer buyers in the market is the condition that facilitates the increase in negotiating power for CMOs.